When we want to kwow if a portfolio or a fund or an ETF is worth investing, we want to kwow if what its average return per unit of risk is so that we can compare and contrast different portfolios for us to make a decision.

Common Decision Making on Investment

Some of the question I ask is whether passive index funds such as VTI or SPY is "the" best investment choice, given its investment strategy, risks or returns.

But what if there are any other funds that can absolutly beet the index funds?

One way to find out is to compare them with VTI or SPY.

Basis of Comparison

So to begin comparing funds, we need to kwow what we are comparing. Is it the historical average returns we are comparing? Is it the volitility of prices we are comparing? Is does not make too much sense if we compare the average return or the volitility seperately right?

For example, if we are looking for the fund with the best mean return of a investment span of 1,000 days, the 3X Bull S&P 500 ETF UPRO is probably one of the best. Source:Performance Comparison Between SPY and UPRO

Well, the time I wrote this article, the stock market is going through some hard times with S&P 500 has dropped more than 20%. I don't think people want to all-in UPRO right now with the fear of possible recession.

Then, here comes the second metric of comparison, the volitility or standard deviation. But If we want the lowest standard deviation, we can just hold on to cash. Cash does not have price volitiliy.

Average return per unit of risk

So then we can divide the average return by the return standard deviaion. We can call it average return per unit of risk.

Now, it is time we find our best funds. So do you what I find the best investment strategy is when comparing annual average return divided by annual return standard deviation?

The answer is iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD). Well, this is just one fund that beats SPY. Maybe there are others.

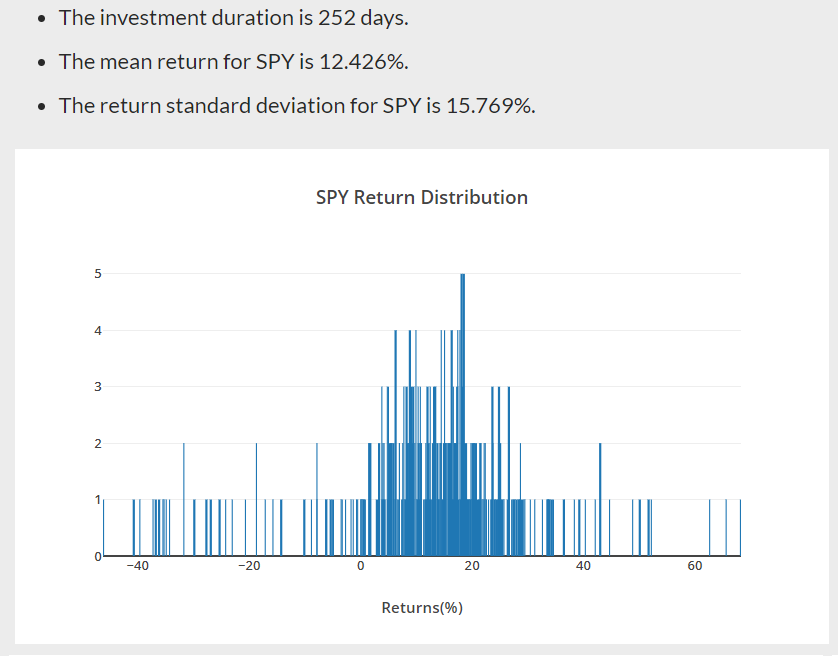

The following comparison data is from 2002/7/30 to 2022/7/1.

- LQD has an average return of 5.908%, standard deviation os 6.87%, the avearge divided by the standard deviation 0.860.

- SPY has an average return of 12.426%, standard deviation os 15.769%, the avearge divided by the standard deviation 0.788.

LQD Annual Return Distribution

SPY Annual Return Distribution

Problem

Just when I am happy with the answer that LQD is absolutly better than SPY, that's when I found out that LQD does not beat SPY in Sharpe ratios.

When I look at the Sharpe ratios of SPY and LQD, despite LQD has a better average return per unit of risk, SPY has a higher Sharpe ratio when the risk free rate is 2% which is the Fed's long-run average inflation target.

- LQD's Sharpe ratio is 0.540.

- SPY 's Sharpe ratio is 0.661.

LQD Sharpe Ratio

SPY Sharpe Ratio

Why in Sharpe Ratio Formula Risk Free Rate has to be take out from Mean Return?

After finding out the above facts, I began thinking why the risk free rate has to be taken out from the average return when calculating the Shrpe ratio and I came up with some hyperthotical data.

Suppose, we keep cash or very short term bonds. Cash has a return of bank's saving interest rate, say 0.1% per year. But it has a 0% standard deviation in returns. You are going to earn the interest with no uncertainty, not -0.1% or 0.2% like most other investment assets, even short term treasury ETF has volitility.

Than if we don't account for the risk free rate in calcuting the Sharpe ratio, we obtain some number that is infinity.

Sharpe ratio for cash = 0.1%/ 0% = infinity

For Sharpe ratio to make some kind of sense, we should subtract 0.1% from the 0.1% definite return of cash in this sceneraio to get

Sharpe ratio for cash = 0.1%/ 0.1% = infinity/infinity

Althogh infinity/infinity is not well defined as the anwser, but it is still better representation of cash's Sharpe ratio.

Why?

Because we can go on with the cash example with 3 year bond which has a higher return than cash when yield curve is not inverted.

With the same logic, say a 3-year US bond has a yield of 1% and no risk when held until maturity.

Sharpe ratio for a 3-year US bond = 1%/ 1% = infinity

We have the same problem with a infinity Sharp ratio.

We can choose something that has a low return but much much lower volatility to get a extremely high Sharpe ratio, because the Sharpe ratio would be meaningless otherwise.

If we go further with investment grade coporate bond such as LQD, we are going to have something with a relatively high Sharpe ratio when we don't take out the risk free rate from the average return in the Sharpe raio formula.

Therefore, it makes more sense we subtrack the risk free when calculating the Sharpe ratio.

What does Sharpe ratio imply?

After considering SPY and LQD, LQD has a better Shapr raito when the risk free rate is 0, SPY has a higher Sharpe ratio otherwise.

Because SPY has an annual average return two times bigger than LQD's, it is time to subtract the risk free rate and divided tham by volitility to obtain some numbers that can better represent the excess return per unit of risk.

Or what this means is SPY is a more efficient assest than LQD in investing in the market and gives more of a fair share of economic growth when volitility is taken into accout.

SPY, IVV, VTI or all other passive index funds work the similar way.

Comments

Post a Comment